For most of modern financial history, the answer to “where do I hide?” was boringly obvious. You bought U.S. Treasuries. You bought gold. You waited out the storm. This was not ideology; it was pattern recognition accumulated over decades of crises, confirmed repeatedly enough that it stopped being questioned and became infrastructure.

What is worth examining today is not whether that trust was misplaced, but whether it requires updating. The world has changed in ways that are not cyclical. Geopolitical alignments that held for a generation are fraying. The U.S. government has demonstrated, more than once in recent years, a willingness to use its financial infrastructure as a political instrument. And the investors quietly responding to these shifts are not hedge funds chasing alpha; they are central banks, sovereign wealth funds, and institutional allocators whose behaviour shapes the very conditions that make a safe haven safe.

This is an important distinction. Safe havens are not safe by nature. They are safe by consensus.

What makes a safe haven safe

To assess whether something still works, it helps to understand why it worked in the first place.

U.S. Treasury bonds earned their safe-haven status through a specific combination of properties that are worth naming precisely. First, liquidity: the Treasury market is the deepest and most liquid in the world, meaning that in a moment of panic, an investor can exit a large position without moving the market against themselves. Second, dollar dominance: because international trade, commodities, and debt contracts are predominantly denominated in dollars, demand for dollar assets is structurally embedded in the global economy. Third, and perhaps most importantly, institutional credibility: the belief, reinforced over decades, that the U.S. government will honour its obligations and that the Federal Reserve will act as a competent steward of monetary stability.

Gold operates on different logic entirely. It is the anti-institutional safe haven. It carries no counterparty risk because it is no one’s liability. It cannot be inflated away, frozen, or defaulted upon. Where Treasuries are safe because of institutions, gold is safe in spite of them; or, more precisely, as a hedge against their failure. This is why the two assets have historically been complementary rather than redundant. Treasuries perform in deflationary crises and liquidity panics; gold performs when confidence in the monetary order itself begins to erode.

Understanding this distinction matters enormously when deciding which safe haven to reach for, and why.

Treasury bonds and gold under crisis: what the evidence shows

The last fifteen years have been unusually generous in providing material for analysis. Four distinct crises have stress-tested the safe-haven thesis under different conditions, and the results are worth sitting with.

In 2008, Treasuries performed flawlessly. As the global financial system teetered on the edge of collapse, capital flooded into U.S. government debt, yields fell sharply, and the narrative was confirmed. But it is worth noting the nature of that crisis: it was a private sector failure. The U.S. government was the solution, not the problem, and confidence in sovereign credit was never remotely in question. The test was designed in a way that Treasuries were almost certain to pass.

The 2020 pandemic shock offered a more complicated picture. In the first weeks of March 2020, as markets sold everything indiscriminately, even Treasuries came under pressure; a jarring development that required Federal Reserve intervention on an extraordinary scale to stabilise. Gold was similarly sold in the initial panic. The lesson was not that either asset had failed, but that in a sufficiently acute liquidity crisis, the first instinct is cash, not safe havens, and that the Fed’s willingness and capacity to act as a backstop is itself a component of Treasury safety that cannot be taken for granted.

The 2022 inflation shock was the most instructive test of all. U.S. Treasury bonds suffered their worst calendar-year performance in modern history, losing over 18% on a total return basis. Investors who had held Treasuries as a defensive position found that “safe” and “inflation-protected” are not synonyms; a distinction that forty years of low inflation had allowed the industry to paper over. Gold, meanwhile, failed to capitalise on the inflationary environment in the way many expected, ending 2022 roughly flat, squeezed between inflation tailwinds and the headwind of rising real interest rates. The episode was a reminder that gold is a better hedge against monetary disorder than against inflation per se.

Then came the post-2022 period, which introduced something qualitatively new.

The sanctions precedent: how geopolitical risk entered the safe-haven equation

When the United States and its allies moved in early 2022 to freeze approximately $300 billion of Russian central bank reserves held in Western financial institutions, the action was legally defensible and strategically rational. It was also, in the quiet assessment of many sovereign wealth managers and central bankers elsewhere, deeply unsettling.

The dollar-based financial system had long operated on an implicit understanding: that access to it was governed by rules, not by politics. The Russian sanctions did not break that understanding outright, but they demonstrated that it was conditional in ways that had never been tested before. For the first time, a G20 nation’s foreign reserves (accumulated over decades precisely as a rainy-day fund) had been rendered inaccessible by political decision rather than by any market mechanism.

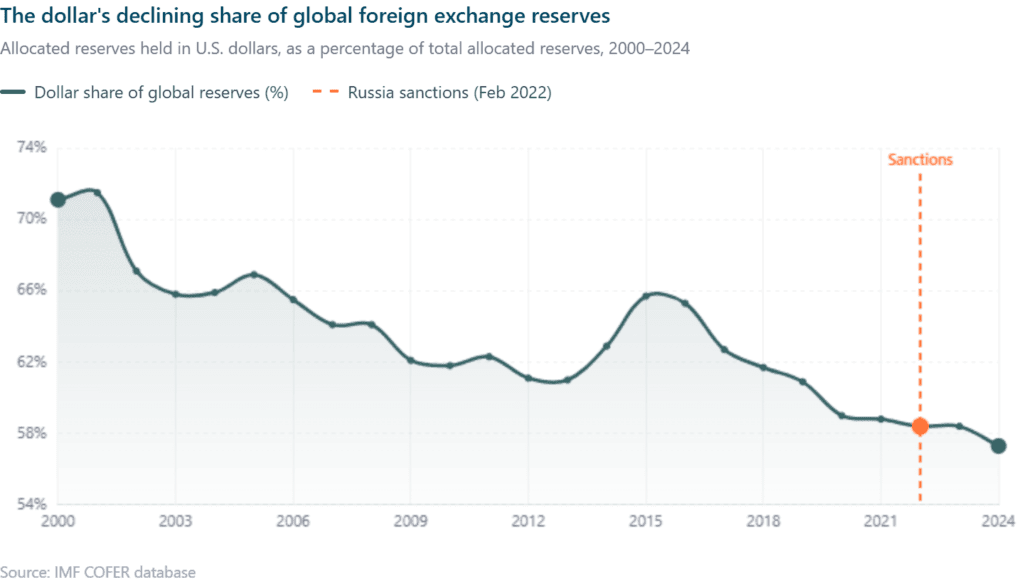

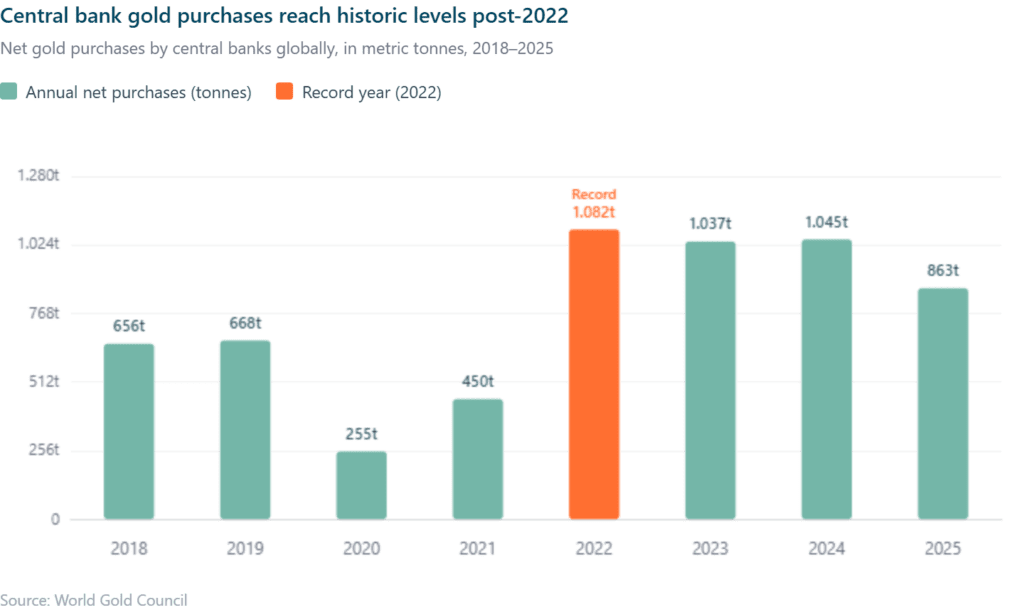

The response has been measured but visible. Global central bank gold purchases reached record levels in 2022 and remained elevated through 2023 and 2024, driven disproportionately by emerging market institutions that had previously been modest buyers. The dollar’s share of global foreign exchange reserves has declined from roughly 70% in 2000 to approximately 57% today. That is not a rout. It is not even, in isolation, alarming. But it is a sustained, directional trend that predates the Ukraine crisis and has accelerated since.

The relevant question is not whether the dollar is losing its reserve currency status; the structural case for dollar dominance remains strong, given the absence of a credible alternative at scale. The question is whether the safe-haven premium embedded in Treasury bonds is stable. And here, the answer is genuinely less certain than it was five years ago. The marginal sovereign buyer of Treasuries is conducting a calculation that now includes a political risk variable that did not previously exist.

For gold, this dynamic is a structural tailwind. Gold cannot be frozen. It does not require a custodian in New York or London. It is, by definition, outside the reach of financial sanctions. That these properties are now being explicitly valued by central bank reserve managers (not just speculative investors) represents a shift in the demand base for gold that is worth taking seriously.

U.S. institutional credibility and the risk investors are slow to price

The geopolitical story is only half of the picture. The domestic institutional story is the more delicate one to tell, because it involves assessing risks that have not yet crystallised into outcomes.

The United States has, over the past decade, introduced a degree of political risk into its sovereign debt that was previously considered implausible. The debt ceiling (a mechanism that most other developed economies manage as a procedural formality) has become a recurring site of brinkmanship, with the government coming close enough to technical default in 2023 to prompt Fitch Ratings to downgrade U.S. sovereign debt. Moody’s, the last of the three major agencies to hold the U.S. at its highest rating, followed in May 2025. The market’s reaction to each downgrade has been notably muted, which tells its own story: investors are not yet pricing sovereign risk into Treasuries in the way they might price it into, say, Italian debt. But credit agencies exist precisely to formalise assessments that markets are sometimes slow to make.

There is also the question of Federal Reserve independence, which functions as the institutional backbone of Treasury safe-haven status. A central bank whose credibility is perceived as politically contingent is a different institution from one that is not. This is not a prediction about the future of U.S. monetary policy. It is an observation that the perception of independence is itself a variable, and one that bears watching.

None of this constitutes a case for abandoning Treasuries. The U.S. institutional framework remains considerably more robust than most of its peers. But “the best house in a complicated neighbourhood” is a different proposition from “the unambiguously safe harbour,” and the distinction carries practical implications for portfolio construction.

Portfolio construction in a polycrisic world: treasuries, gold, and TIPS

The case for Treasury bonds and gold as safe havens has not collapsed. It has differentiated. And that differentiation, once understood, becomes a tool rather than a problem.

Treasuries remain the correct response to a deflationary crisis, a banking panic, or a sudden global demand for dollar liquidity. In those scenarios (which remain more probable than their alternatives in any given year) the depth, liquidity, and institutional backing of the Treasury market is without peer. An investor who abandons Treasuries entirely on the basis of long-term structural concerns is likely to find themselves poorly positioned in the next conventional crisis.

Gold’s role has grown more important, and for reasons that are structural rather than speculative. It hedges the scenarios that Treasuries do not: monetary disorder, institutional erosion, geopolitical fragmentation, and the weaponisation of financial infrastructure. These risks have not historically been central to a well-constructed portfolio for a Western investor. They are becoming more relevant.

Inflation-linked Treasury securities (known as TIPS) address the gap that 2022 exposed, offering protection against the scenario in which inflation is the crisis. They are not without complexity: their real yields have at times been deeply negative, and their performance depends on the credibility of the inflation indices they reference. But they fill a hole in the traditional safe-haven framework that nominal Treasuries cannot.

The portfolio implication is less about changing the assets held and more about holding them with a clearer understanding of what each one is actually hedging. A Treasury allocation that has never been stress-tested against an inflation scenario, or a gold allocation that is sized as though sovereign risk is a remote abstraction, reflects assumptions that the world is no longer fully supporting.

Why safe havens can shift faster than fundamentals

There is a philosophical observation worth making at the end of this analysis, because it is relevant to how one holds these conclusions.

Safe havens are, at their core, coordination mechanisms. They are safe because enough people believe them to be safe, and act accordingly. That self-reinforcing quality is both their strength and their vulnerability. When the consensus shifts (even partially, even at the margin) the dynamics can change faster than the fundamentals would suggest. The rise of gold as a preferred reserve asset among central banks is, in part, a story about a shift in that consensus. It is worth watching not because it signals imminent crisis, but because it is the kind of slow-moving structural change that tends to matter a great deal and receive too little attention until it suddenly receives too much.

The question investors should carry forward is not whether Treasuries and gold still work as safe havens in the age of polycrises. They do, under the right conditions. The more useful question is whether they know which conditions they are hedging against (geopolitical fracture, institutional erosion, inflation, or liquidity panic) and whether their portfolio reflects that knowledge with any precision.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own due diligence or consult with a financial advisor before making any investment decisions.

Photo by Weliton Soranzo on Unsplash.